What is the CMHC Eco Plus Program?

The CMHC Eco Plus program is a Canadian federal incentive that helps make energy efficient homes more affordable by offering a partial refund on your mortgage loan insurance premium. When you buy or build a new home that is energy efficient and financed with CMHC-insured mortgage loan insurance, you could receive 25 percent of your mortgage insurance premium back. Even if your mortgage is insured by a private insurer and not CMHC, there’s a good chance your insurer has the same program under another name. There is also a CMHC program for existing housing stock – see below.

Mortgage loan insurance is typically required in Canada when your down payment is less than 20 percent of the purchase price. It protects the lender and enables buyers to qualify with lower down payments. The Eco Plus program rewards buyers for choosing homes that go beyond minimum national energy performance.

This isn’t just a program for the best of the best either – we aren’t talking net-zero and passive homes only. All homes built in BC since 2023 have been required to be 20% more efficient than “a typical new house”. This is worth looking into for everyone purchasing a home (including condos) that require mortgage insurance.

Who Qualifies for the Eco Plus Rebate?

To qualify for the CMHC Eco Plus rebate:

• The home must be financed with CMHC mortgage loan insurance

• The property must be a newly built home that has never been occupied

• The home must meet recognized energy efficiency standards, such as an EnerGuide rating OR an eligible third-party certification like ENERGY STAR, R-2000, LEED, or Passive House, depending on current CMHC criteria. An EnerGuide rating label showing that the home is 20% more efficient than a “typical new home” will suffice.

• You must have paid the CMHC mortgage insurance premium and then apply for the rebate within 24 months of your mortgage closing date

How the Eco Plus Rebate Works

Here’s the simple version of how it works:

- Buy or build a qualifying home: The home must be newly constructed (never occupied before) and have certifiction from an eligible program, or obtain an EnerGuide Label demonstrating the home’s superior efficiency.

- Have a CMHC-insured mortgage: This means you’ve already paid for your mortage insurance and are now applying for a refund of 25%.

- Get energy documentation: A certified EnerGuide rating or eligible certification proves your home’s efficiency. (an NRCan registered Energy Advisor will complete this)

- Apply within 24 months: After your mortgage closes, you have up to two years to submit your Eco Plus application with your energy documentation.

- Receive your refund: If approved, CMHC sends you a refund equal to up to 25 percent of the premium you paid.

For many buyers, this refund can amount to thousands of dollars back in cash, even after considering the cost of the EnerGuide Evaluation being around $600.

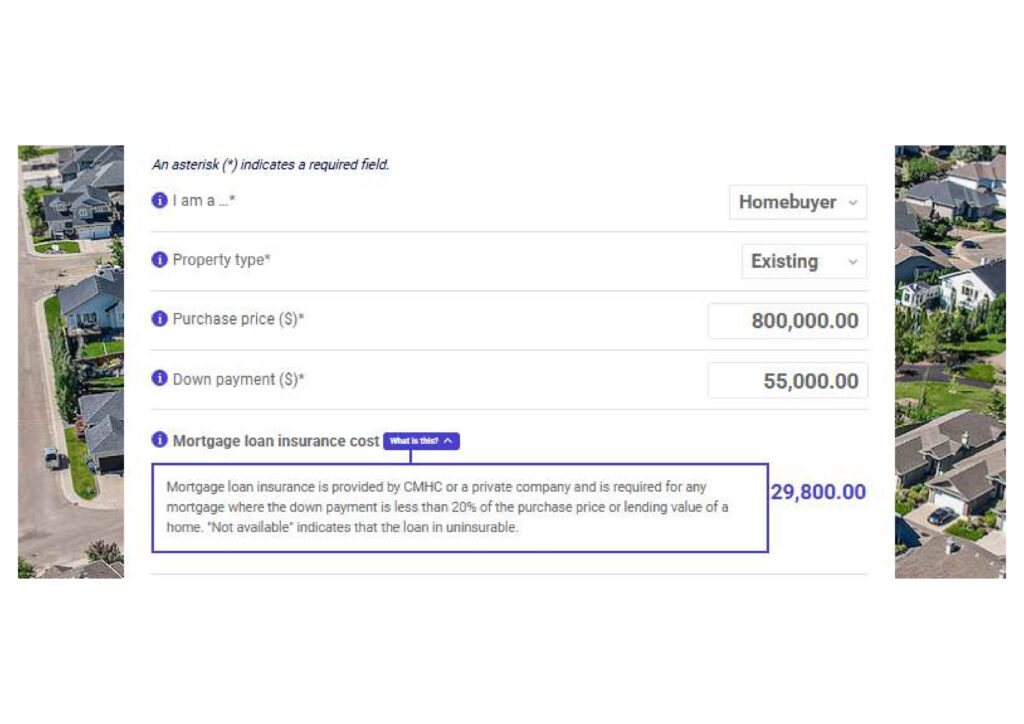

Let’s look at some math:

On a home with a purchase price of $800,000 and minimum downpayment:

Down payment: minimum required on $800,000 = $55,000

• Mortgage amount: $800,000 − $55,000 = $745,000

• CMHC premium: $29,800

This means you could be looking at a mortgage insurance premium refund of ($29,800 x 0.25)= $7,450.

After the cost of your EnerGuide Evaluation (if you don’t already have the documentation you need), that’s almost $7,000 back in your pocket.

Why Energy Efficiency is a bonus on top of the Rebate

Investing in an energy efficient home does more than qualify you for the mortgage insurance rebates. These homes typically:

• Have lower monthly energy costs

• Feature modern heating, cooling, and insulation systems

• Offer more comfort and consistent indoor temperatures

• Reduce environmental impact over time

The rebate helps offset upfront costs and reinforces the long-term savings of efficient design.

Similar Mortgage Insurance Programs

Here are the active mortgage loan insurance refund programs related to energy efficiency that are available to homebuyers in British Columbia:

• Sagen Canada calls its version of Eco-Plus the Energy Efficient Housing Program (EEHP). The application can be found here.

• Canada Guaranty has its Energy Efficient Advantage Program, which also mirrors the CMHC Eco-Plus Program. The application can be found here.

What About Refund Incentives for Existing Housing Stock?

I had this question too. Why all the focus on new homes when there’s so much existing housing stock that would benefit from an Energy Efficiency focus?

Well, here’s CMHC’s answer to that:

CMHC Eco Improvement Program for Existing Homes

In addition to the Eco Plus program for new homes, the Canada Mortgage and Housing Corporation offers the Eco Improvement program to support energy efficient upgrades in existing homes. Under this program, homeowners can receive a partial refund of their mortgage loan insurance premium when they complete eligible energy performance improvements.

To qualify for the Eco Improvement refund:

• The home must be owner-occupied and insured through a current CMHC mortgage.

• The energy performance upgrade must be significant and verifiable, typically involving improvements to the building envelope (insulation, windows, air tightness) or high-efficiency mechanical systems (heat pumps, efficient water heating, etc.).

• You must provide documentation of the completed upgrades and resulting energy performance, often through third-party verification such as an EnerGuide evaluation or equivalent proof of efficiency gains.

• The refund application must be submitted to CMHC within 24 months of your mortgage closing date.

This program requires a minimum spend on energy efficiency improvements of $20,000. That’s a significant bill, I won’t refute that. I am, however, aware of a lot of homeowners in the Okanagan in the last few years who installed heat pumps for around this price range (and may have subsequently received a $10,000 FortisBC rebate). Also, there are a lot of homeowners who installed a solar array for around this price point and would already be eligible.

The Eco Improvement program encourages deeper home performance upgrades. Its intent is to help offset part of the upfront cost through a mortgage insurance refund while also delivering long-term energy savings and reduced operating costs. This program can be especially valuable for homeowners investing in comprehensive retrofits that move their property toward higher energy efficiency.

Tips for Buyers, Homeowners and Builders

If you’re planning to take advantage of the any of the above-mentioned programs:

• Get your EnerGuide rating or certification well in advance of the 24 month deadline after closing.

• Verify your mortgage is CMHC-insured. Did you put less than 20% down on your newly constructed home? If yes, you were required to be covered by CMHC mortgage insurance.

• Submit your application on time: Applications must be sent to CMHC or other mortgage insureres within 24 months of your mortgage closing.

• Work with an energy advisor: A registered energy advisor can help ensure your home meets the required standards and guide you through rating and documentation. Sometimes your home already has the documentation you’ll need without any extra costs needing to be incurred. If you have questions: reach out.

Conclusion

These mortgage insurance refunds offer a valuable way to reduce the cost of mortgage insurance when you choose an energy efficient home or create one after its purchase. By understanding the eligibility requirements, getting the right documentation, and applying within the timeline, you can put thousands of dollars back in your pocket.

If you’re thinking about buying, renovating up to or building an energy efficient home and want help navigating these rebate programs, just ask.

You could receive thousands of dollars back for doing upgrades you were going to do anyway, or maybe have already done, as well as just for buying a new house or condo.